Mortgage Investment Corporation - Questions

Mortgage Investment Corporation - Questions

Blog Article

Indicators on Mortgage Investment Corporation You Should Know

Table of ContentsNot known Details About Mortgage Investment Corporation Fascination About Mortgage Investment CorporationGetting The Mortgage Investment Corporation To WorkThe 5-Minute Rule for Mortgage Investment CorporationThe 8-Minute Rule for Mortgage Investment Corporation

Does the MICs credit history committee testimonial each home loan? In a lot of situations, home mortgage brokers manage MICs. The broker ought to not serve as a participant of the credit rating board, as this places him/her in a direct dispute of rate of interest considered that brokers normally earn a compensation for placing the home loans. 3. Do the directors, participants of credit scores board and fund manager have their own funds spent? An of course to this concern does not supply a risk-free financial investment, it needs to supply some increased protection if examined in combination with other prudent financing policies.Is the MIC levered? Some MICs are levered by a monetary establishment like a chartered financial institution. The financial organization will certainly accept certain mortgages had by the MIC as safety for a line of credit report. The M.I.C. will after that borrow from their credit line and provide the funds at a greater rate.

It is vital that an accountant conversant with MICs prepare these declarations. Thank you Mr. Shewan & Mr.

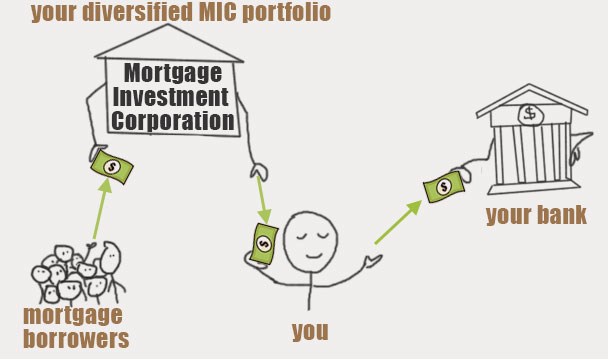

Last updated: Upgraded 14, 2018 Few investments are financial investments advantageous as a Mortgage Investment Home mortgage (Company), when it comes to returns and tax benefits. Since of their company structure, MICs do not pay revenue tax and are legitimately mandated to distribute all of their revenues to investors.

This does not suggest there are not dangers, yet, normally talking, whatever the more comprehensive securities market is doing, the Canadian property market, especially significant cities like Toronto, Vancouver, and Montreal executes well. A MIC is a corporation created under the rules establish out in the Income Tax Obligation Act, Area 130.1.

The MIC gains revenue from those mortgages on rate of interest costs and basic fees. The genuine charm of a Mortgage Investment Firm is the return it provides investors contrasted to other set earnings financial investments. You will certainly have no trouble finding a GIC that pays 2% for an one-year term, as federal government bonds are similarly as reduced.

Mortgage Investment Corporation - An Overview

There are stringent demands under the Income Tax Act that a company must satisfy before it certifies as a MIC. A MIC has to be a Canadian firm and it have to invest its funds in home mortgages. In fact, MICs are not enabled to manage or create property building. That said, there are times when the MIC ends up possessing the mortgaged residential property because of foreclosure, sale arrangement, etc.

A MIC will gain interest revenue from mortgages and any kind of money the Web Site MIC has in the financial institution. As long as 100% of the profits/dividends are provided to investors, the MIC does not pay any kind of earnings tax obligation. Rather than the MIC paying tax on the interest it makes, shareholders are responsible for any tax.

The Basic Principles Of Mortgage Investment Corporation

And Deferred Strategies do not pay any tax obligation on the interest they are approximated to receive - Mortgage Investment Corporation. That claimed, those that hold TFSAs and annuitants of RRSPs or RRIFs may be hit with specific fine tax obligations if the investment in the MIC is considered to be a "restricted financial investment" according to copyright's tax code

They will ensure you have discovered a Home loan Financial investment Company with "professional financial investment" condition. If the MIC certifies, maybe extremely valuable come tax obligation time considering that the MIC does not pay tax obligation on the rate of interest income and neither does the Deferred Strategy. More extensively, if the MIC fails to meet the demands laid out by the Earnings Tax Obligation Act, the MICs earnings will be strained prior to it gets distributed to shareholders, reducing returns substantially.

It shows up both the property and stock exchange in copyright are at perpetuity highs On the other hand returns on bonds and GICs are still near document lows. Also cash money is shedding its charm due to the fact that power and food rates have actually pressed the inflation rate to a multi-year high. Which pleads the inquiry: Where can we still discover value? Well I assume I have the answer! In May I blogged concerning exploring home mortgage financial investment firms.

See This Report about Mortgage Investment Corporation

Many effort Canadians who intend to buy a residence can not get mortgages from traditional banks since possibly they're self utilized, or do not have a recognized credit score background yet. Or discover this perhaps they desire a brief term finance to create a big residential or commercial property or make some improvements. Banks have a tendency to ignore these possible borrowers because self used Canadians don't have secure revenues.

Report this page